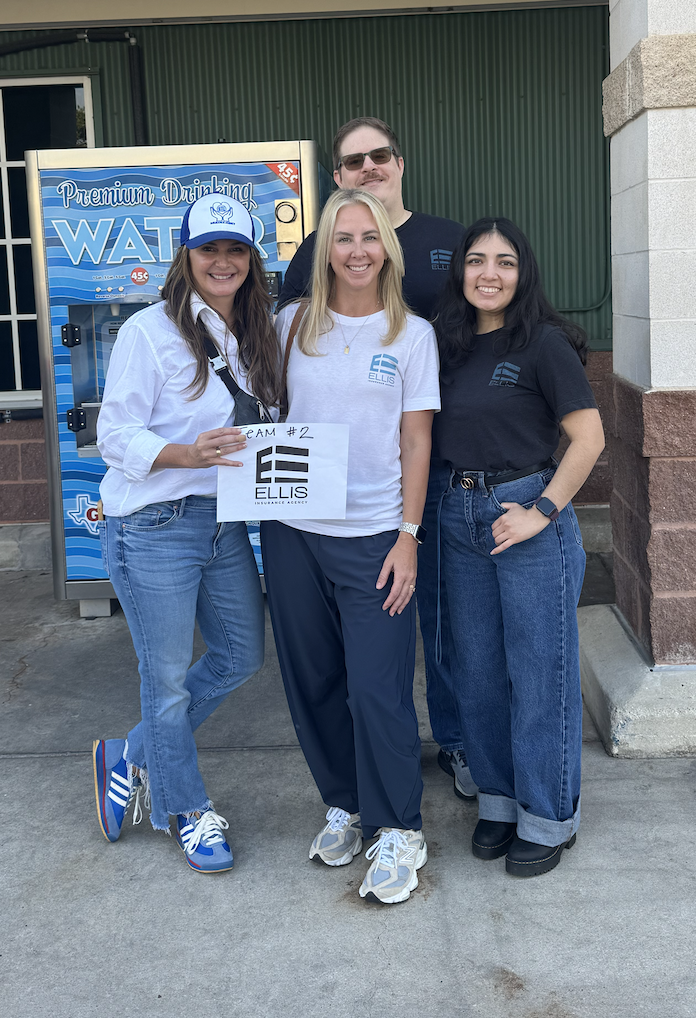

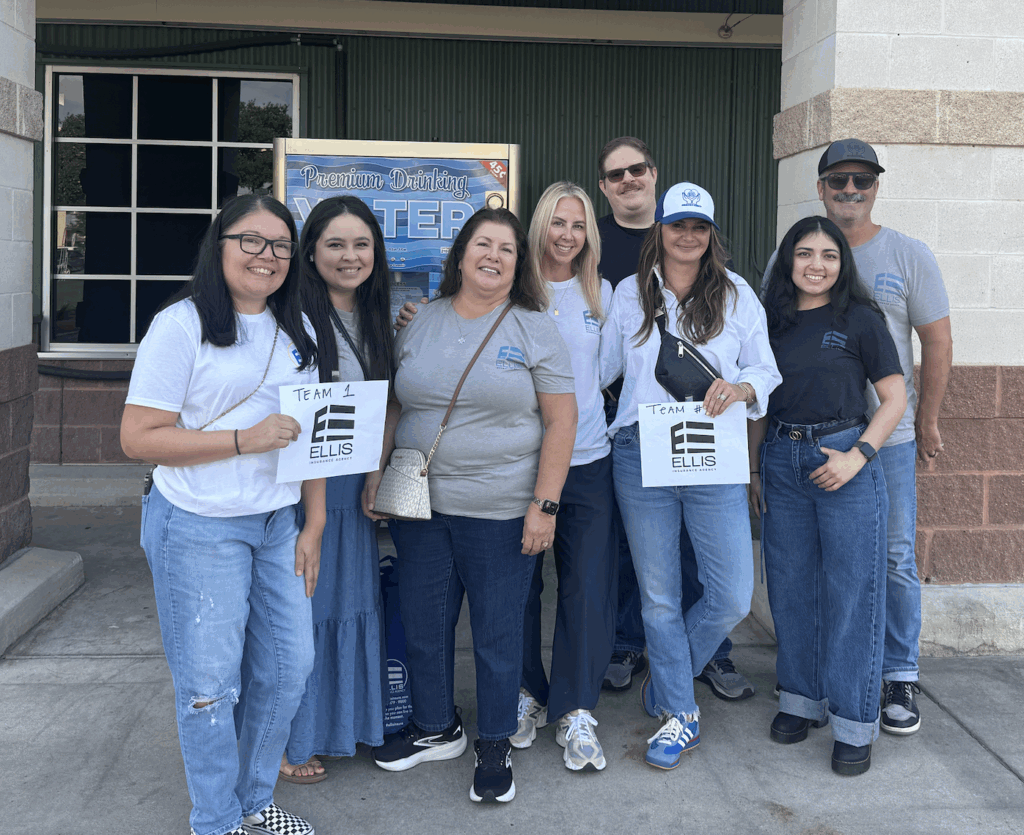

At Ellis Insurance Agency, giving back to our community isn’t just something we talk about; it’s part of who we are. Recently, we had the opportunity to partner with Safeco/Liberty Mutual in a unique and meaningful way, turning a business accomplishment into an unforgettable act of service.

As part of our ongoing collaboration, Safeco/Liberty Mutual challenged us to reach certain business goals. When we achieved them, instead of accepting the reward for ourselves, we decided to do something different. Something bigger. Something fun.

Introducing… the EIA Grocery Games! With the support of Safeco/Liberty Mutual, our team brainstormed a creative and energetic way to give back: a Grocery Games contest! We split into two teams here at EIA and headed to our local H-E-B to shop for a cause, focusing on purchasing the items most needed on the SA Food Bank’s list.

The rules were simple:

Each team had to get as close to $500 as possible — without going over.

It was fast, it was competitive, and it was a blast.

In the end, both teams came incredibly close, and together we purchased $1,000 worth of food, totaling 480 pounds — all donated directly to the San Antonio Food Bank.

A First in Texas

We’re proud to share that Ellis Insurance Agency is the only agency in Texas to give back their business-goal reward in this way. Because of this, the Safeco/Liberty Mutual team joined us in-store, filming and photographing the entire experience. They plan to share a highlight reel soon, so stay tuned!

A Heartfelt Thank You

We couldn’t have done this without our amazing EIA family who brings passion and purpose to everything we do. And a huge thank you to our partners at Safeco/Liberty Mutual for embracing our idea and helping us make a real impact while having a whole lot of fun in the process.

Community matters. Creativity matters. And at EIA, we’re proud to continue leading with both.

Stay tuned for the video and thank you for supporting Ellis Insurance Agency!

San Antonio, TX, August 2025 – Ellis Insurance Agency has earned the 2025 Best Practices Agency status, joining an elite group of independent insurance agencies from across the United States.

The Best Practices Agency designation is awarded to participants in the Best Practices Study, which analyzes and documents the business practices of the highest-performing insurance agencies in the industry.

This year, 1,146 independent agencies throughout the U.S. were nominated to compete for this coveted designation and only 348 agencies scored high enough to qualify as a Best Practices Agency.

“This is a testament to our dedicated team who spend countless hours providing the best service to our wonderful (and loyal) clients. We are humbled by this honor and will continue to work hard for the clients we help protect.” – Lee Gamel, President

Since 1993, the Independent Insurance Agents & Brokers of America (IIABA or the Big “I”) and Reagan Consulting, an Atlanta-based management consulting firm, have joined forces to study the country’s leading agencies in seven revenue categories.

Best Practices Agencies are selected every three years through a rigorous nomination and qualifying process. Each agency must be among the 35-45 top-performing agencies in its revenue category to be awarded Best Practices status.

Best Practices Agencies retain their status annually during the three-year cycle by submitting extensive financial and operational data for review. 2025 is the first year of the current three-year study cycle.

Ellis Insurance Agency was founded in 1980 and can offer insurance products from a number of different companies you can see HERE.

For further information, please contact Lee Gamel of Ellis Insurance Agency at 210-979-9000.

Founded in 1993, Reagan Consulting provides M&A advisory, capital raising, valuation, growth consulting, perpetuation planning, and industry research to the nation’s leading insurance brokerages.

Founded in 1896, the Independent Insurance Agents & Brokers of America (the Big “I”) is the nation’s oldest and largest national association of independent insurance agents and brokers, representing over 25,000 agency locations united under the Trusted Choice brand. Trusted Choice independent agents offer consumers all types of insurance — property, casualty, life, health, employee benefit plans, and retirement products — from various insurance companies.

When most people think about their homeowners or commercial property insurance, they assume “flood” is automatically covered. Unfortunately, that’s not the case and learning this after water is rising in your living room or business can be a devastating (and costly) surprise.

Flood coverage is almost never included in standard homeowners or property insurance policies. Instead, it must be purchased separately, either through the National Flood Insurance Program (NFIP) or from a private flood insurer.

Whether you own a home, a business, or both, here’s what you need to know to protect yourself before the next heavy storm rolls in.

What Exactly Counts as a “Flood”?

In insurance terms, a flood isn’t just any water damage. It has a very specific definition:

A general and temporary condition where two or more acres of normally dry land—or two or more properties — are inundated by water or mudflow.

That means water damage from a burst pipe or a leaky roof is not considered a flood. But storm surge, heavy rain overflow, river swelling, or flash flooding from sudden downpours often meet the definition.

What is a Flood Zone?

Flood zones are geographic areas defined by FEMA (Federal Emergency Management Agency) to indicate different levels of flood risk:

· High-Risk Zones (A or V): These have at least a 1% annual chance of flooding (also called the “100-year flood”). Lenders usually require flood insurance here.

· Moderate-to-Low-Risk Zones (B, C, X): Flooding is less likely, but still possible. About 25% of flood claims come from these areas.

· Undetermined Risk Zones (D): Flood hazards are possible, but not mapped.

Why You Still Need Flood Insurance in a Low-Risk Zone

Many homeowners skip flood insurance because their lender doesn’t require it. But here’s the truth:

· Flooding can happen anywhere — it’s the most common and costly natural disaster in the U.S.

· Just one inch of water can cause $25,000 or more in damage.

· Federal disaster assistance is not guaranteed and often comes in the form of loans you must repay.

Questions to Ask When Considering Flood Insurance

1. Is my property in a FEMA-designated flood zone?

2. What’s the cost difference between NFIP coverage and private flood insurance?

3. Does my policy cover the replacement cost or actual cash value?

4. What are the coverage limits for my building and personal/business property?

5. Is there a waiting period before coverage starts? (NFIP policies typically have a 30-day wait.)

6. Are there exclusions I should be aware of? (For example, basements often have coverage limitations.)

7. Can renter’s purchase flood insurance? Renter’s can purchase flood insurance, but only in the NFIP. The NFIP offers a Contents-Only policy covering personal belongings (furniture, clothing, electronics) up to $100,000.

Key Details to Look for in a Flood Policy

· Coverage Limits: NFIP policies max out at $250,000 for residential structures and $500,000 for commercial buildings, plus limited contents coverage. Private insurers may offer higher limits.

· Contents Coverage: Check if it’s included or requires a separate policy.

· Deductibles: Understand how much you’ll be responsible for if you file a claim.

· Waiting Period: Factor in the time before the policy takes effect—don’t wait until a storm is approaching.

The Bottom Line

Flood insurance isn’t just for people living on the coast or near rivers. It’s for anyone who wants peace of mind that their home or business is protected from one of nature’s most damaging (and unpredictable) forces.

Don’t wait for the next big storm to start asking questions. Review your coverage now, understand your flood risk, and explore your options for protection.

Need help figuring out your flood risk or finding the right policy?

Ellis Insurance Agency can walk you through your options, compare NFIP and private flood coverage, and ensure you’re protected before the water rises.

What is a payment schedule in roof insurance claims?

A Payment Schedule is a specific method used by most insurance companies to determine the settlement amount for a damaged roof. Unlike Actual Cash Value (ACV) or Replacement Cost (RC) settlements, this approach does not rely on the current market value or full replacement cost of the roof. Instead, it applies a predetermined percentage reduction based on the roof’s age at the time of the loss. The older the roof, the greater the reduction in the payout. This method is designed to offer a consistent and transparent settlement process for both the homeowner and the insurer.

How does the payment schedule work?

The Payment Schedule follows a sliding scale, meaning the amount you’re eligible to receive for roof damage decreases as your roof gets older. Here’s a simplified example to illustrate how this might work—note that this is just a general example and not an official payment schedule from any specific insurance company: • Roof Age 0–5 years: 100% of the replacement cost • Roof Age 6–10 years: 80% of the replacement cost • Roof Age 11–15 years: 60% of the replacement cost • Roof Age 16–20 years: 40% of the replacement cost • Roof Age 21+ years: 20% of the replacement cost

Keep in mind that the exact percentages and age brackets can vary widely depending on your insurance provider and policy. The key takeaway is that the older your roof is, the lower the payout you can expect under a Payment Schedule approach.

The Process of a Payment Schedule Claim

Damage Assessment: Once you report roof damage, an insurance adjuster will inspect the roof to evaluate the extent of the damage and estimate the replacement cost.

Age Verification: The adjuster or insurance company will verify the age of your roof, typically requiring documentation such as installation records or receipts.

Payment Calculation: Using the Payment Schedule, the insurance company applies a percentage based on your roof’s age to the estimated replacement cost. For example, if your roof has a replacement value of $20,000 and is determined to be 6 years old, you may receive 80% of that value, or $16,000.

Settlement: The final payout is issued after subtracting your home insurance deductible. This amount is intended to help cover the cost of repairing or replacing your roof.

Advantages and Considerations

Advantages: • Predictability: Homeowners have a clear understanding of what percentage of the roof replacement cost they might receive, based on the roof’s age. • Perceived Fairness: The approach seeks to strike a balance between providing coverage for homeowners and managing risk for the insurance company.

Considerations: • Reduced Payouts for Older Roofs: Homeowners with aging roofs may receive significantly lower settlements compared to Replacement Cost (RC) policies, especially if the roof was already near the end of its useful life. • Policy Differences: Not all insurers offer a Payment Schedule option, and those that do may use widely varying age brackets and payout percentages. It’s important to review your specific policy details carefully.

In conclusion…

A Payment Schedule in roof insurance claims provides a structured, age-based method for determining settlement amounts after roof damage. Unlike Actual Cash Value or Replacement Cost policies, this approach reduces the payout according to the age of the roof, offering homeowners a predictable and transparent understanding of what they can expect. While it can be seen as a fair way to balance the insurer’s risk and the homeowner’s coverage, it often results in lower payouts for older roofs. Because Payment Schedules and their specific terms can vary greatly between insurance providers, it’s essential for homeowners to review their policies closely and understand how their roof’s age could impact a future claim.

Insurance companies run credit-based insurance scores as part of their assessment process because these scores are seen as indicators of an individual’s financial responsibility and potential risk. Studies have shown a correlation between credit-based insurance scores and the likelihood of filing insurance claims. Individuals with lower insurance scores are statistically more likely to file claims, which can lead to higher costs for insurers. By using insurance scores, insurers aim to predict and mitigate potential risks, ensuring that they can set premiums that accurately reflect the likelihood of future claims. This practice allows insurers to price their policies more effectively, offering lower premiums to those with better insurance scores who are perceived as lower risk, while charging higher rates to those with lower scores to account for the increased likelihood of claim activity.

It is important to note that these companies use credit-based insurance scores rather than traditional credit scores, which means requesting an insurance quote will not hurt your credit score. An article on FICO.com provides a more detailed explanation of the differences between a credit score and an insurance score. Please click HERE to learn more.

Understanding how insurance companies utilize credit-based insurance scores can help consumers navigate the insurance landscape more effectively. While these scores are a tool for predicting potential risk, they also highlight the importance of maintaining good financial habits, as credit scores can influence not only loan rates but also insurance premiums. Insurance companies do offer exceptions to credit-based insurance scoring if you were the victim of identity theft or another qualifying life event, please click HERE to learn more. By leveraging credit data, insurers can offer more accurate pricing, rewarding financially responsible individuals with lower premiums. For more insights into how insurance scores differ from traditional credit scores, be sure to check out the detailed explanation on FICO.com.

Read below to learn more about New Texas Vehicle Inspection laws starting January 1, 2025, Hurricane Helene update and hurricane preparedness, and the difference between an Insurance Agency vs. Insurance Company.

New Texas Vehicle Inspection Law

Starting January 1, 2025, Texas will eliminate the requirement for annual safety inspections for most non-commercial vehicles, as part of House Bill 3297. This means vehicle owners will no longer need to visit inspection stations for annual checks. However, a $7.50 fee, known as the “inspection program replacement fee,” will still be applied during vehicle registration. The collected fees will support state funds such as the Texas Mobility Fund and the Clean Air Account.

Despite the elimination of the safety inspections, vehicles in certain counties, including Harris, Fort Bend, and Montgomery, will still be required to undergo annual emissions testing to ensure compliance with environmental regulations. Commercial vehicles, however, are not affected by these changes and will still need to complete annual inspections.

Hurricane Helene made landfall on the night of September 26, 2024, in Florida’s Big Bend area as a powerful Category 4 storm. With sustained winds of 140 mph, the storm caused widespread damage, particularly along the northwestern coastline. Officials issued warnings about life-threatening storm surges, which resulted in catastrophic flooding, while hurricane-force winds knocked out power to nearly a million homes and businesses. Florida Governor Ron DeSantis and other southeastern states declared states of emergency as the storm’s impact extended into Georgia and the Carolinas.

For detailed guidance on staying safe during hurricane season, check out our previous blog on hurricane preparedness. It covers essential tips and strategies to help you protect your home and family before, during, and after a storm.

Insurance Agency vs. Insurance Company

An insurance agency and an insurance company serve distinct roles in the insurance market. An insurance agency acts as an intermediary between customers and insurance companies. Agencies represent multiple insurers and work to find the best policies for their clients, tailoring coverage options to meet individual needs. They essentially sell and manage policies on behalf of insurance companies.

An insurance company, on the other hand, is the entity that underwrites and provides the insurance policies. It assumes the financial risk, collects premiums, and is responsible for paying out claims. While agencies focus on selling and servicing policies, insurance companies are the ones that create and back the coverage financially.

Referrals and Reviews

Referrals and Google reviews are key to our business growth by boosting credibility and expanding our reach. Referrals provide trusted, word-of-mouth endorsements, while positive Google reviews increase online visibility and showcase the quality of our services. Together, they build trust, attract new customers, and drive sustainable growth through customer acquisition and retention.

Property insurance in Texas (and in most states in the US) continues to challenge the insurance industry – inflation, large weather-related claims, inconsistent weather patterns, material and labor increases have found their way into all our premiums. 2023 added another layer of complexity in Texas as many of the insurance companies tightened up restrictions on where and what kind of homes they want to cover. One of the biggest areas of focus (and rating factors) for property insurance is the age of our roofs. Many insurance companies are now requiring proof of roof age, this proof comes in several forms:

Roofing Permit or Certificate (typically from a licensed roofer and/or roofing company)

Paid receipt showing roof replacement (and scope of work done)

Pre-purchase inspection (hold on to these if you have recently purchased a home)

Roof Inspection completed within the last 6-12 months, including photos showing all sides of the roof

When it comes to commercial insurance, our team has you covered. We are excited to introduce our newest member, Veronica, who brings a wealth of expertise to our team. Learn more about Cyber Security and its importance for your small business, as safeguarding your digital assets is crucial in today’s landscape. Additionally, explore whether your company requires commercial auto insurance to protect your vehicles and drivers. To foster a productive work environment, check out an article written by our friend and client, Levi Kirwin, on creating clarity and communication throughout your organization, where we discuss effective strategies to enhance transparency and engagement within your team. In our Client Center, we offer personalized assistance to address your specific needs, ensuring you get the most comprehensive coverage.

Meet Our Newest Commercial Lines Account Manager

Introducing Veronica Caesarez, our newest Commercial Lines Account Manager. With over 20 years of experience in the insurance industry, she brings a wealth of knowledge to our team. Learn more about Veronica and our other amazing team members HERE.

Do you need Commercial Auto Insurance?

Are you unsure whether your business needs commercial auto insurance? Progressive Insurance has published an insightful article that clearly outlines the differences between personal and commercial auto insurance. This resource can help you determine whether your business vehicles require commercial coverage to ensure you’re adequately protected on the road. Check it out to make an informed decision tailored to your specific needs.

Creating Clarity and Communication Throughout Your Organization

1 Point, 2 Minutes: Energize your teams through communicating consistent clarity of purpose.

Founders and CEOs need to answer six questions to create clarity and communicate clarity consistently throughout your organization (see Patrick Lencioni’s “The Advantage”)

Why do we exist?

“Because the world needs…” (fill in your WHY)

How do we behave?

Define core values, no more than five.

What do we do?

Your one sentence value proposition for prospects.

How will we succeed?

What are the unique(s) your product or service brings to the market?

What is most important, right now?

The time horizon should be from 3-12 months.

This choice you make should be exactly ONE thing that, if accomplished, will move your firm forward more than any other choice.

Outline one sentence as a thematic goal, and define objectives in clear steps as work tasks.

Connect these to your business goals for the year. Revenue, prospect pipeline strength, cost reduction, something else.

WHO must do WHAT to accomplish the most important choice you have identified?

This isn’t a prompt to Ctl-C, Ctl-V your org chart.

Instead, you are assigning each clearly defined work task to exactly one owner to accomplish “what is most important.”

Get your leadership team aligned and agreed on (1) – (6). Congratulations, you have created clarity! Now, communicate clarity. Create a short simple communication for (5) and (6) for each team leader to cover, each week, on progress to the goal. Repeat clarity. Every week.

You’re the visible leader and you set the rhythm of your organization; you set the pulse by your words and presence. You cannot, you CANNOT, repeat this enough in your daily interactions with your team. You will feel like you are repeating yourself in annoying ways. But each of your team only hears you a small fraction of his or her day. Your words frame the day, maybe the week, when your team hears you. Communicate what you want them to remember.

Clarity galvanizes your marketing strategy, your prospecting and sales processes, and your operational muscle towards one goal, one vision, One Point on the horizon to run towards. Help them keep their eyes on the prize. It’s your responsibility. Executing well is how you win the year.

Ready to create clarity for your team, prospects, and customers?

Levi Kirwin, founder of Nissi Revenue Generation, translates founders’ and CEO’s vision for conquest into marketing strategy, brand storytelling, and sales process execution.

Levi Kirwin | 813-424-7812 | nissirg@proton.me

Cyber Security and It’s Importance to Your Small Business

Last week’s CrowdStrike software update resulted in outages for millions of Microsoft Windows users, potentially costing the economy billions of dollars and triggering cyber policy claims for numerous businesses worldwide. Today’s businesses depend on technology to thrive. However, with the benefits of technology come increased risks. Now is the time to review your current cyber insurance coverage. Determine which policies provide coverage, check notice of loss requirements, limitations, and any other coverage considerations. Watch this video from Central Insurance to learn how to protect your small business from a cyber attack.

Inspection Recommendations

Inspection recommendations have become increasingly crucial as Excess and Surplus (E&S) carriers have tightened their inspection protocols. To ensure compliance and secure the necessary coverage, it’s important to adhere to these stricter guidelines. By following detailed inspection recommendations, businesses can avoid potential coverage issues and maintain the high standards required by E&S carriers, ultimately protecting their assets and operations more effectively. Watch this VIDEO by Fusco Orsini & Associates Insurance Services X 4C to learn more!

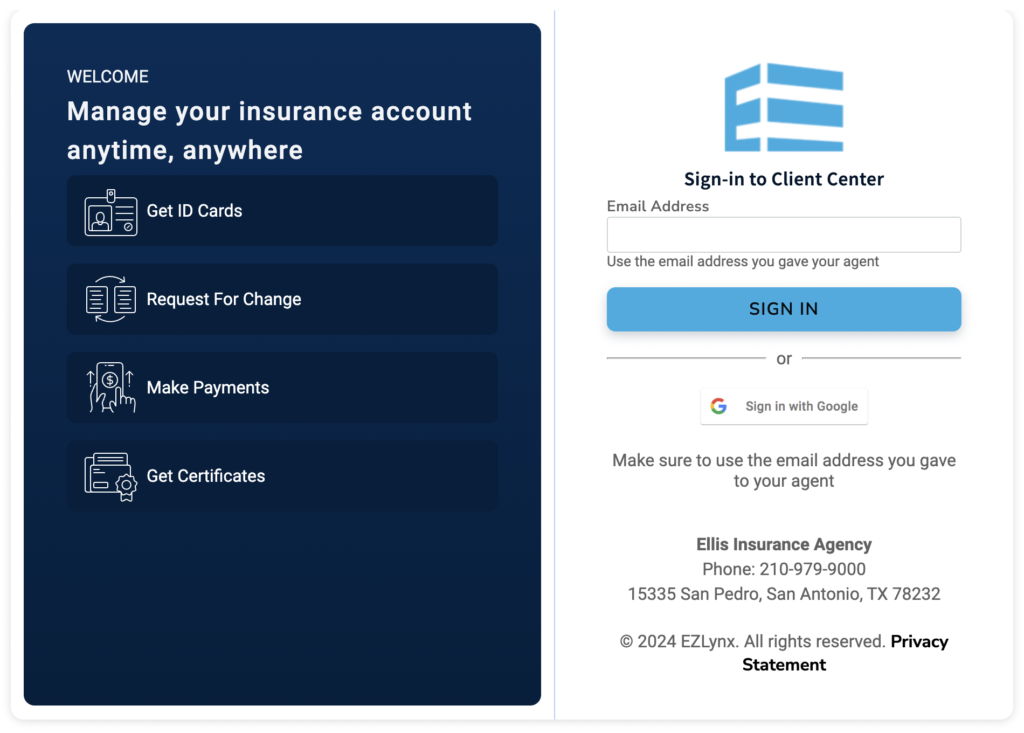

Ellis Insurance Agency Client Center

Did you know about our digital customer service? You can use our Client Center to view your insurance policies, make payments, print insurance ID cards, update your contact information, download documents, and more!

School is OUT and Summer is HERE! Read on to learn more about Hurricane Season, the top car models stolen in 2023, and how your referrals and Google reviews help our business!

Hurricane Season

Hurricane season is June 1st through November 30th. Learn more about hurricane preparedness and what to do in the event of a flood/natural disaster.

Hurricane Preparedness

A hurricane can be a devastating force of nature whether you live inland or on a coast. Being prepared can potentially help save you, your family, and your home from permanent damage. Read on to see what steps you can take to prepare for this hurricane season.

Evaluate Your Risk

Living on the coast is a higher probability to being hit by a hurricane, but inland residents are also at risk. Heavy rains, winds, and storm surges can cause wind damage and flooding. Once you evaluate your location and review historical hurricane information, you can decide whats best for you to prepare.

Preparing Your Family

You and your family’s safety is essential. Follow this guide to ensure you have a plan in place in the event of a hurricane

Develop an evacuation plan.

Prepare for power outages. Flashlights, electric lanterns, and gas-powered generators are a great place to start.

Build an emergency kit. Click here to find a list of basic emergency supplies to have on hand.

Be sure to secure important documents in a fire/water proof safe.

Preparing Your Home

While preparing your family and their safety is most important, it is good to start preparing your house before hurricane season starts. Here are some tips for preparing the exterior of your home.

Check window and door seals. It’s important that these are in good condition to prevent water damage inside your home.

Install storm shutters (if you’re in a high-risk area) or have boards available to put over your windows.

Trim tree branches around your roof. High winds can cause trees and branches to damage your home.

Clean your gutters to help water flow and prevent roof damage.

Make sure you garage door(s) are secure.

Have sandbags available to divert water from your home if you are in a high-risk area.

Now that your home and your family are prepared, be sure to check with your insurance agent to review your home policy. Most homeowners insurance will cover wind damage, but not flood damage as flood insurance is a separate policy. Be sure to ask what the best steps will be in the event that you need to file a claim after a hurricane. You can track current hurricanes and tropical storms by visiting the NOAA tracking site. Stay prepared and safe!

Top Stolen Car Models in 2023

Hyundai and Kia: Among the Top 10 Most Stolen Cars in 2023

In 2023, Hyundai and Kia vehicles made headlines for an unfortunate reason—they were among the top 10 most stolen cars in the United States. This surge in thefts has brought significant attention to these popular brands, prompting concerns among car owners, manufacturers, and law enforcement agencies.

The Rise in Thefts

The increase in thefts of Hyundai and Kia vehicles can be attributed to several factors. A primary reason is the relative ease with which certain models can be stolen. Many Hyundai and Kia cars manufactured between 2011 and 2021 lack engine immobilizers, a standard feature in most modern vehicles that prevents the engine from starting without the correct key. This omission has made these vehicles particularly vulnerable to theft through techniques as simple as breaking a window and manipulating the ignition.

Social Media Impact

Another surprising catalyst for the spike in thefts has been social media. Videos demonstrating how to steal these cars have proliferated on platforms like TikTok and YouTube, providing would-be thieves with step-by-step instructions. This phenomenon has not only increased the number of thefts but also highlighted the vulnerability of these vehicles to a global audience.

Impact on Owners and Communities

The rise in thefts has had significant repercussions for car owners and communities. Many Hyundai and Kia owners have reported increased insurance premiums and difficulty securing coverage due to the high risk of theft. Communities, especially in urban areas, have seen a notable uptick in car theft-related crimes, straining local law enforcement resources and fostering a sense of insecurity among residents.

Manufacturer Response

In response to the surge in thefts, Hyundai and Kia have taken several measures to address the issue. Both companies have expedited the implementation of engine immobilizers in their newer models to enhance security. Additionally, they have provided software updates and security kits for older models to make them less susceptible to theft.

Moreover, Hyundai and Kia have collaborated with law enforcement agencies to raise awareness about the theft risk and educate owners on preventive measures. They have also offered steering wheel locks and other anti-theft devices to affected customers at no charge, aiming to mitigate the immediate risk while longer-term solutions are developed.

Legal and Regulatory Actions

The theft epidemic has also spurred legal and regulatory responses. Several cities and states have called for stricter regulations and standards for vehicle security to prevent such vulnerabilities in the future. There have been discussions about potential class-action lawsuits against the manufacturers for failing to equip their vehicles with adequate anti-theft technology, reflecting the growing frustration among consumers and policymakers.

Looking Ahead

While Hyundai and Kia have taken significant steps to address the theft issue, the long-term impact on their reputation remains uncertain. The companies’ swift response and commitment to enhancing vehicle security are positive signs, but restoring consumer confidence will likely require sustained effort and innovation.

As the automotive industry continues to evolve, the Hyundai and Kia theft phenomenon underscores the importance of robust security measures in vehicle design. For car manufacturers, it serves as a crucial lesson in the necessity of keeping pace with technological advancements and emerging threats to ensure the safety and security of their customers.

In conclusion, the inclusion of Hyundai and Kia vehicles in the list of the top 10 most stolen cars in 2023 has spotlighted critical vulnerabilities in vehicle security. Addressing these challenges head-on, both manufacturers and regulatory bodies must work together to prevent such issues from recurring in the future, ensuring safer streets and greater peace of mind for car owners everywhere.

Referral Program and Google Reviews

Referrals and Google reviews play a crucial role in boosting our business by enhancing our credibility and expanding our customer base. Referrals from satisfied clients provide powerful word-of-mouth endorsements that build trust and encourage potential customers to choose our services. Meanwhile, positive Google reviews improve our online visibility, making it easier for people to find us when searching for relevant services. These reviews also serve as testimonials to the quality of our work, influencing potential clients’ decisions and fostering a sense of community trust. Together, referrals and Google reviews create a virtuous cycle of customer acquisition and retention, driving sustainable business growth.

Thank you for trusting Ellis Insurance Agency – We love our clients!

Our team and families are grateful for the nice, cooler weather. Read on to learn more about Home and Auto rate increases, meet our two newest team members, and our latest Commercial Spotlight!

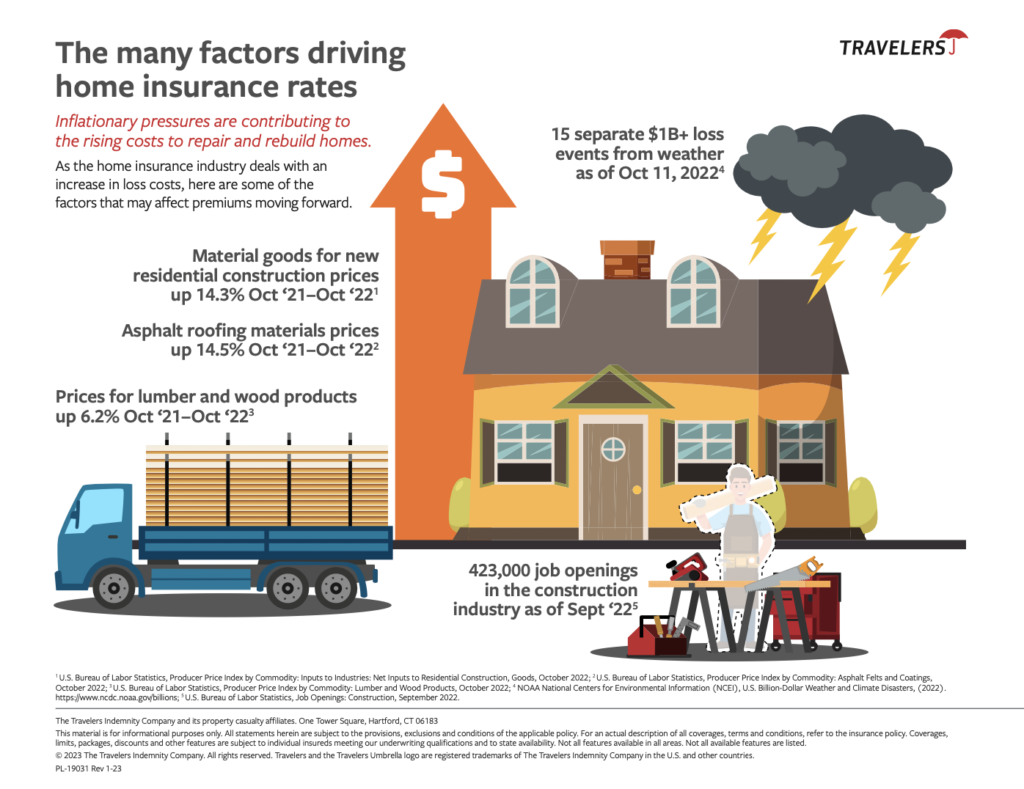

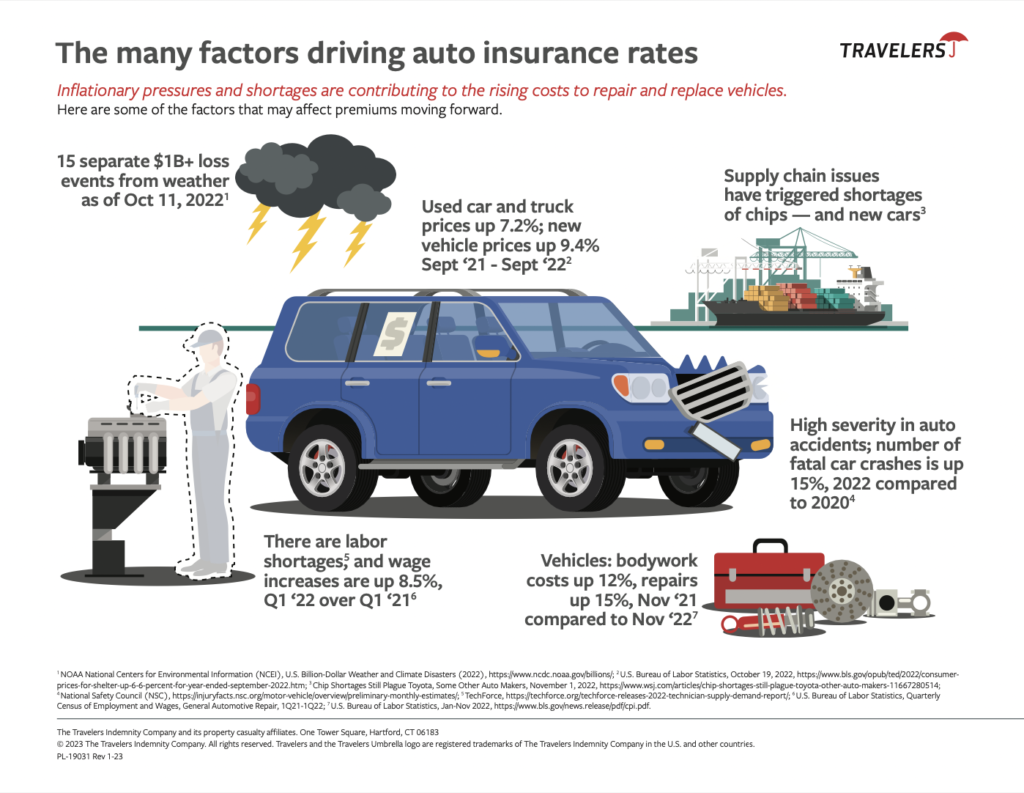

Understanding Home and Auto Rate Increases

Thanks to Travelers Insurance, we wanted to share two visuals to help you understand why we’ve seen rate increases in Home and Auto insurance.

We hope these visuals can help you understand some of the reasons for rate increases. If you have any questions about your policy/policies, please feel free to call your agent! We are here to help.

Welcome to the team!

We are excited to expand our team to create a better experience for our clients. Please welcome Yvonne and Mary Lou!

Yvonne joins our commercial team as a Commercial Account Manager. Check out her proudest moment and what she does to stay “zen” by clicking HERE!

Mary Lou came on as a Client Service and Sales Consultant for our Personal Lines team. She has been in the business for 20+ years and loves the outdoors! Find out more about MaryLou by clicking HERE!

Commercial Spotlight

Our most recent Commercial Spotlight was Statesman Hair Restoration and Aesthetics. They specialize in hair transplant right here in San Antonio. Their microscopic analysis lets them see underneath the scalp to determine the root of the problem. Hair loss can be caused for many reasons, so if you or anyone you know are experiencing hair loss or thinning, Statesman offers FREE consults. You can visit their website by clicking HERE.

Referral Winners – July and August

Did you know that for every referral you send to us, your name is entered in for a chance to win a $100 Amazon gift card for that month? Yes! It’s true! We are so thankful for our clients and appreciate your referrals and reviews. Had a good experience? Let us know! Thank you to our 2023 July and August client referral winners:

Laura Guerrero-Redman

David Dullnig

EIA Thanks you for your trust and support. We love our clients!

Have you had a great experience? Feel free to leave us a Google review!